All content was accurate at the time of publication. Check issuer’s site for most up to date information.

katiestraveltricks.com has partnered with CardRatings for our coverage of credit card products. katiestraveltricks.com and CardRatings may receive a commission from our partners. American Express is a katiestraveltricks.com advertiser. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. For Capital One products listed on this page, some of the above benefits are provided by Visa® or Mastercard® and may vary by product. See the respective Guide to Benefits for details, as terms and exclusions apply.

How to Open Business Credit Cards (even if you don’t have a business)

Business cards offer substantial points bonuses for new cards. Don’t skip these cards because you don’t think of yourself as a business owner. You might be, from the perspective of a bank. Applying for a business credit card is easier than you might think — see the step by step instructions here.

This article is updated frequently to include new information.

How to qualify for a business card

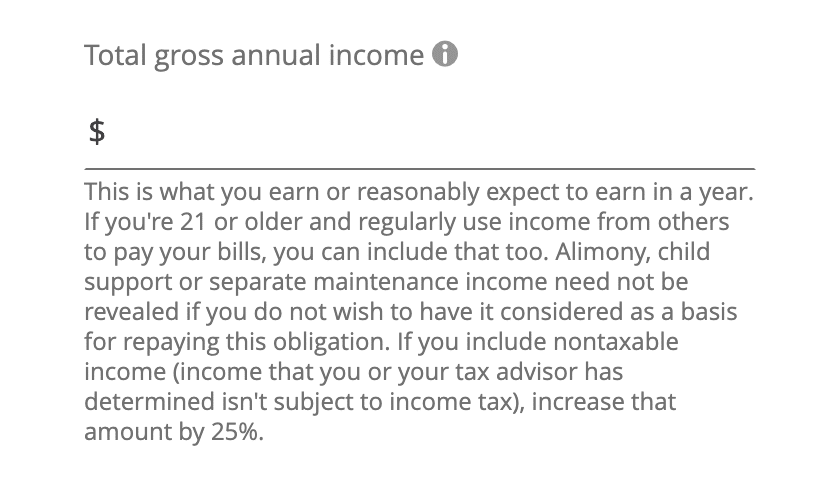

If you earn money through any sort of side hustle, you probably can qualify for a business card. That’s because you can be considered a “sole proprietor” with a small business from the perspective of the bank.

We own and rent out a condominium and apply for business cards for our rental property business. When we travel, we sometimes rent out our house via Airbnb, so we have other business cards for that business. I’ve talked to friends who sell (even sparingly) on eBay or Facebook Marketplace or craigslist and apply for cards for their resale businesses. One even applied by listing $100 annual income from her garage sale business and got approved. If you freelance or tutor or consult or babysit or drive for Uber you probably qualify, too.

The most important thing is to be honest on your application about your business revenue. If you make $200 a year selling your kids’ old clothes on Facebook Marketplace, just put $200 when it asks for revenue on the application. You can also watch my YouTube video for more details on this.

What are the tax implications?

Generally speaking, there are no tax implications for opening a business card.

The IRS isn't notified that you have opened a business credit card or told how much or what you charge to the card.

If you already have a side hustle that earns more than $600 per year, you may already receive a 1099 form for that anyway, but this won't have any direct relationship with any business credit cards you've opened.

You can apply as a sole proprietor and use your Social Security Number as a Tax ID. Or you can apply for a free EIN from the IRS.

Why business cards should be a key part of your overall points strategy

Why do I bother even mentioning business cards? There are two big reasons: access to more great offers and reducing the number of cards on your personal credit report.

Increased offers

Having a small business will open the door to a lot more offers for you. Honestly, I think the offers are so great that if I didn't already have a few side hustles, I would be motivated to start one just to access the deals.

The ability to open business cards more than doubles your card options and earning potential because it adds so many more card offers you can apply for.

Opening business cards doubles your card options

Helps your credit score

Next, generally speaking, business cards don't affect your personal credit report. This helps keep your credit score higher if you want to apply for cards and cancel them after one year.

There is an important caveat for business cards from Capital One which are generally reported to your personal credit report with the exception of a few including the Capital One Venture X Business credit card.

Because business cards generally don't show up on your personal credit report, they also make it easier to get approved for more cards from more banks.

Keeps you under 5/24 longer

If you're working on slowly applying for cards from Chase, you can mix in business cards from Chase and other banks without affecting your 5/24 score.

My favorite business card offers

If you apply for a card, I appreciate when you use my affiliate links! It costs you $0 to use but helps support the site and allows me to keep creating resources.

Chase Ink Cards

The Chase Ink Business Cash® Credit Card and Chase Ink Business Unlimited® Credit Card will list their bonus as cash back. But there's an important loophole here for you to learn! These cards technically earn Chase Ultimate Rewards® points that can "only be redeemed for cash back." If you also have a Chase Sapphire card, you also earn Chase Ultimate Rewards® points. The UR connected to your Sapphire card are more powerful because they can be transferred to partners like Hyatt and United which can unlock some sweet value.

If you have both a Chase Sapphire Preferred® Card and Chase Ink Business Unlimited® Credit Card or Chase Ink Business Cash® Credit Card — Chase will let you move the Chase Ultimate Rewards® from the "cash back" card over to the Sapphire — and they gain the ability to transfer to partners! The same principle works with the Chase Freedom cards which are no annual fee personal cards.

Katie's Take

Why this card might (or might not) be right for you.

Show

Hide

Katie's Take

Why this card might (or might not) be right for you.

A perennial favorite! No annual fee and you can convert the cash back > Ultimate Rewards if you also have a card like the Chase Sapphire Preferred® Card

Highlights

The key benefits and earning rates at a glance.

Show

Hide

Highlights

The key benefits and earning rates at a glance.

-

Complimentary 3-Month Instacart+ Membership + $20/Month Instacart Credit (Through Dec 31, 2027) 3 months of complimentary Instacart+ membership plus $20 in Instacart credits each month through December 31, 2027 while you have Instacart+.

-

Move Cash Back into Ultimate Rewards Points Cash back is technically Chase Ultimate Rewards points ($1 cash back = 100 UR points). When paired with a Chase Sapphire (Preferred, Reserve, or Reserve Business) or Ink Business Preferred, you can combine points for transfers to 14+ airline and hotel partners — including World of Hyatt, United, Air Canada Aeroplan, Southwest, JetBlue, and more.

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

Show

Hide

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

| Offer | Spend Req. | Date |

|---|---|---|

| $750 Cash Back | $6,000 in 3 months | Standard (current as of May 1, 2026) |

| $900 Cash BackElevated | $6,000 in 3 months | Best-ever; ran September 12 - November 13, 2025 |

| $900 Cash BackElevated | $6,000 in 3 months | Returned September 2023 - mid-January 2024 |

| $900 Cash BackElevated | $6,000 in 3 months | Fall 2022 |

| $750 Cash Back | $7,500 in 3 months | Pandemic-era offer |

| $500 Cash Back | $3,000 in 3 months | Long-running historical standard |

Katie's Take

Why this card might (or might not) be right for you.

Show

Hide

Katie's Take

Why this card might (or might not) be right for you.

A perennial favorite! No annual fee and you can convert the cash back > Ultimate Rewards if you also have a card like the Chase Sapphire Preferred® Card

Highlights

The key benefits and earning rates at a glance.

Show

Hide

Highlights

The key benefits and earning rates at a glance.

-

Complimentary 3-Month Instacart+ Membership + $20/Month Instacart Credit (Through Dec 31, 2027) 3 months of complimentary Instacart+ membership ($99/year value) plus $20 in Instacart credits each month when you have Instacart+ through December 31, 2027.

-

Move Cash Back into Ultimate Rewards Points Cash back is technically Chase Ultimate Rewards points ($1 cash back = 100 UR points). When paired with a Chase Sapphire (Preferred, Reserve, or Reserve Business) or Ink Business Preferred, you can combine points for transfers to 14+ airline and hotel partners — including World of Hyatt, United, Air Canada Aeroplan, Southwest, JetBlue, and more.

-

0% Intro APR on Purchases (12 Months) 0% intro APR on purchases for 12 months from account opening. After that, a variable APR applies

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

Show

Hide

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

| Offer | Spend Req. | Date |

|---|---|---|

| $750 Cash Back | $6,000 in 3 months | Standard (current as of May 1, 2026) |

| $900 Cash BackElevated | $6,000 in 3 months | Best-ever; ran September 12 - November 13, 2025 |

| $900 Cash BackElevated | $6,000 in 3 months | Fall 2024 (mid-September to early November) |

| $900 Cash BackElevated | $6,000 in 3 months | Returned September 2023 - mid-January 2024 |

| $900 Cash BackElevated | $6,000 in 3 months | Fall 2022 |

| $750 Cash Back | $7,500 in 3 months | Pandemic-era offer |

| $500 Cash Back | $3,000 in 3 months | Long-running historical standard |

Katie's Take

Why this card might (or might not) be right for you.

Show

Hide

Katie's Take

Why this card might (or might not) be right for you.

Overall good card option for earning Ultimate Rewards. One of the few that still earns 3x on travel.

Highlights

The key benefits and earning rates at a glance.

Show

Hide

Highlights

The key benefits and earning rates at a glance.

-

Cell Phone Protection (Up to $1,000/Claim) Get up to $1,000 per claim in cell phone protection against covered theft or damage when you pay your monthly cell phone bill with the card. Maximum 3 claims per year, $100 deductible per claim.

-

Complimentary DashPass + $10/Month DoorDash Grocery Credit (Through Dec 31, 2027) Complimentary access to DashPass by DoorDash for a minimum of one year (activate by 12/31/2027). Includes $0 delivery fees and reduced service fees. Plus, $10/month statement credit on DoorDash grocery and retail orders.

-

Auto Rental Collision Damage Waiver (PRIMARY for Business Rentals) Primary auto rental collision damage waiver coverage for business rentals. Charge the entire rental cost to your card and decline the rental company's CDW.

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

Show

Hide

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

| Offer | Spend Req. | Date |

|---|---|---|

| 100,000 Bonus Points (ELEVATED)Elevated | $8,000 in 3 months | Current ELEVATED offer; available online since early January 2026 |

| 80,000 Bonus Points | $8,000 in 3 months | Standard baseline offer |

| 90,000 Bonus Points | $8,000 in 3 months | Standard offer for most of 2025 |

| 100,000 Bonus Points (Older) | $15,000 in 3 months | Older offer with higher spend requirement |

| 120,000 Bonus Points (BEST-EVER)Elevated | $8,000 in 3 months | Best-ever; ran July - early September 2024 |

Southwest® Rapid Rewards® Performance Business Credit Card

Katie's Take

Why this card might (or might not) be right for you.

Show

Hide

Katie's Take

Why this card might (or might not) be right for you.

Steep annual fee but might be worth it to help you earn a Companion Pass.

Highlights

The key benefits and earning rates at a glance.

Show

Hide

Highlights

The key benefits and earning rates at a glance.

-

9,000 Bonus Points on Each Cardholder Anniversary Receive 9,000 Rapid Rewards bonus points each cardmember anniversary year. Worth approximately $126.

-

Preferred Seat Selection at Booking + Extra Legroom Upgrades 48hr Before Departure Select a Preferred or Standard seat at booking, when available, for cardholder + up to 8 passengers on same reservation. Plus, free upgrade to Extra Legroom seat within 48 hours prior to departure when available.

-

Up to $120 Global Entry / TSA PreCheck® / NEXUS Statement Credit Statement credit of up to $120 every 4 years as reimbursement when you pay for Global Entry, TSA PreCheck® or NEXUS application fee.

-

First Checked Bag Free First checked bag free for cardmember and up to 8 additional passengers in the same reservation.

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

Show

Hide

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

| Offer | Spend Req. | Date |

|---|---|---|

| 80,000 Bonus Points | $5,000 in 3 months | Standard (current as of May 1, 2026) |

| 80,000 Bonus Points | $5,000 in 3 months | Long-running standard since launch |

| 120,000 Bonus Points + Promotional Companion PassElevated | $10,000 in 3 months | Peak elevated; ran in Spring 2025 and Spring 2026 |

Southwest® Rapid Rewards® Premier Business Credit Card

Katie's Take

Why this card might (or might not) be right for you.

Show

Hide

Katie's Take

Why this card might (or might not) be right for you.

This would be my choice of business card -- as long as the math works out and still allows you to earn a Companion Pass.

Highlights

The key benefits and earning rates at a glance.

Show

Hide

Highlights

The key benefits and earning rates at a glance.

-

6,000 Bonus Points on Each Cardholder Anniversary Receive 6,000 Rapid Rewards bonus points each cardmember anniversary year. Worth approximately $84.

-

Standard or Preferred Seat Selection 48hr Before Departure Select a Standard or Preferred seat within 48 hours prior to departure, when available, for cardholder + up to 8 passengers on same reservation.

-

15% Flight Discount Promo Code Receive a 15% promo code each cardmember anniversary year. Can be used for Choice fares and above.

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

Show

Hide

Offer History

See past welcome bonuses to gauge whether the current offer is elevated.

| Offer | Spend Req. | Date |

|---|---|---|

| 60,000 Bonus Points | $3,000 in 3 months | Standard (current as of May 1, 2026) |

| 120,000 Bonus Points (60K + 60K tier)Elevated | $3,000 + additional $12,000 in 3 months | Elevated; ran in Summer 2023 |

| 120,000 Bonus Points (60K + 60K tier)Elevated | $3,000 + additional $15,000 in 3 months | Best-ever; ran in Summer 2024 |

Lower spend options: Cards from Barclays

Barclays often has great business card offers that require a relatively low spend to earn a bonus. Barclays is most likely to approve you if you have opened 6 cards or fewer in the past 24 months. They also sometimes flag an application and will require you to go through a rigamarole like sending in paper copies of your driver's license to get the account approved.

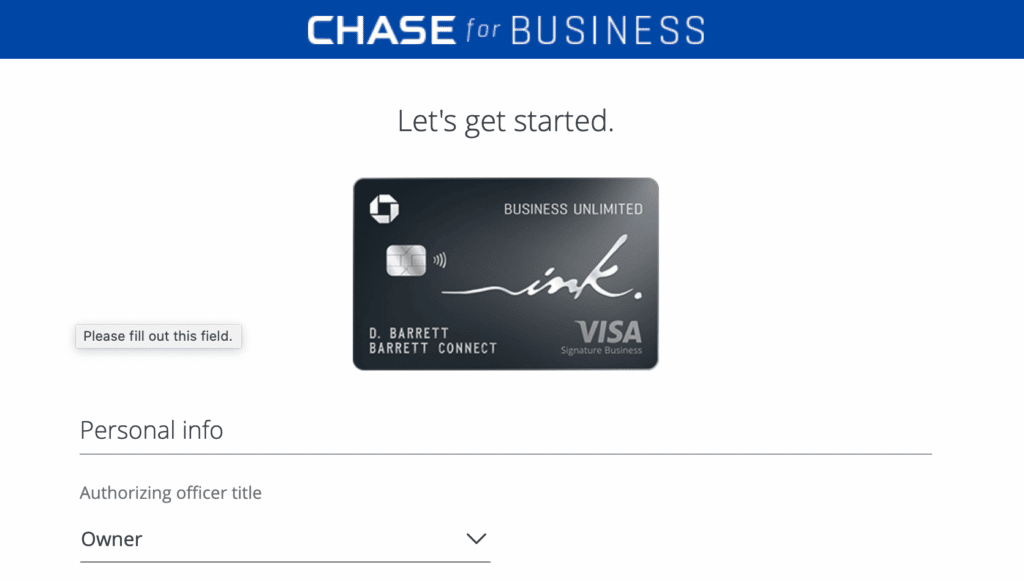

Applying for a Business Credit Card: Tips

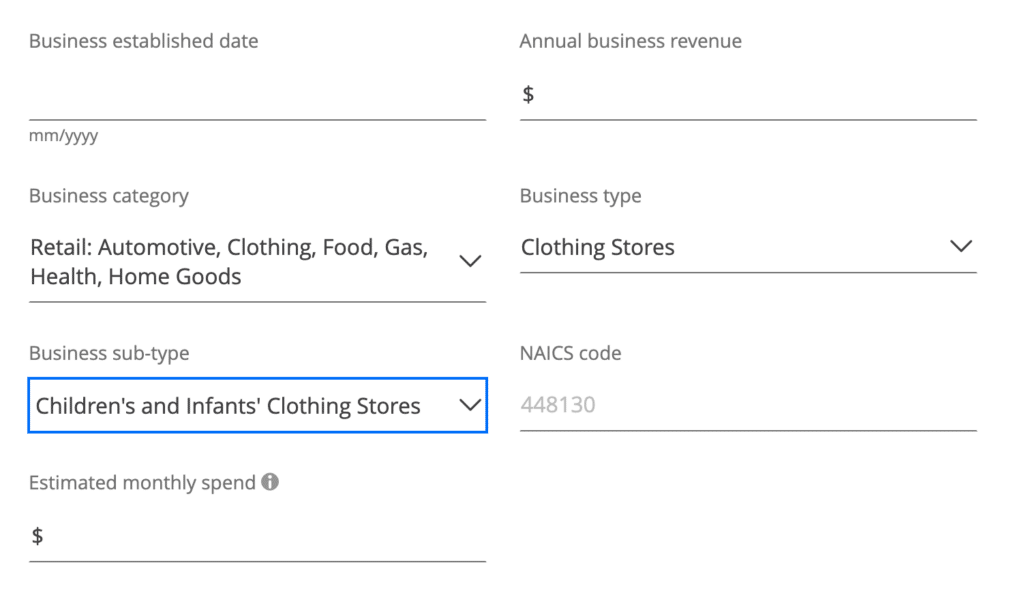

Screenshots of Chase Business Credit Card Application

You will likely be a sole proprietor

How long does it take to get approved?

Sometimes you will get instant approval. After you submit your application, your approval may be confirmed.

Other times, the bank may need more time to review your application. After this review, they may auto-approve you, or they may request additional documents. Because of this, it can take up to 30 days for the bank to make a decision.

What happens if I put personal expenses on a business card?

First, if you have a small business with a bookkeeper that keeps track of expenses, you'll need to sort this out with them!

Most banks will require you to attest that you will be using your new business account "only for business purposes and not personal, family or household purposes."

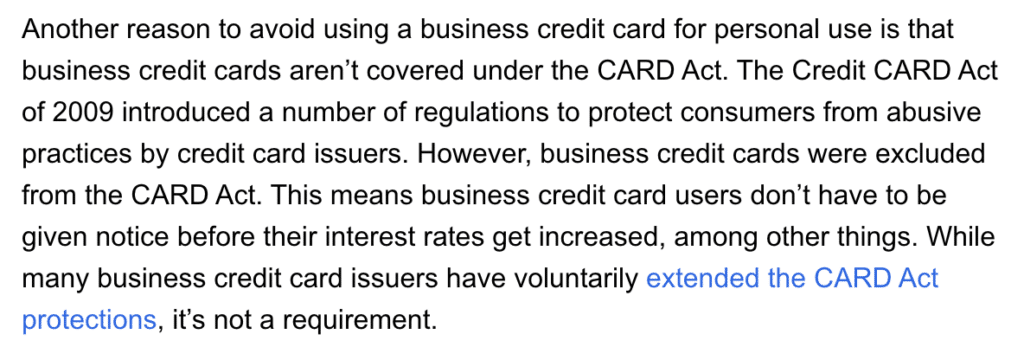

While it isn't illegal to put personal expenses on a business credit, banks are required to ask you to use it for business expenses only. That's due to the CARD Act which extended new protections to consumer credit cards but not business cards.

How to link your Chase business and personal accounts

If you have both business and personal accounts with a bank, you may have to create separate logins for the business cards and personal cards. This can be annoying when you are monitoring your cards and are having to log in and log out of your accounts.

Chase has simplified linking your accounts and now allows you to do this online by following these steps. While you still will have a separate business and personal login, you can easily link your accounts online so you can see everything in one place.

Table of Contents

Related Posts

Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

If you put personal expenses on a business card, you will be liable for the debt. Depending on the card issuer and the type of card, you may be held personally liable for any debt accrued on the card, regardless of whether it is for business or personal use. Additionally, the card issuer may revoke the card and cancel your account if you misuse the card for personal purposes. to use it for personal expenses, you may also be liable for any taxes due from the personal use of the card.

Can I apply for multiple business cards and get multiple Sign-Up Bonuses. I’m thinking 2 cards, 2 different businesses that are both sole proprietor owned? I currently have an Ink Business Unlimited and would like to get another for a different business.

Yes absolutely!

Can I apply for two of the same Ink cards at the same time if I use a different structure for each? — Apply for one card as a sole proprietor using my SS# and then apply for a 2nd card as an LLC using my EIN?

You could but generally Chase will only approve one business card every 30 days.

I thought I read earlier in a different article if you have a big expense coming up open up a card. So if we pay for my daughter’s completion dance up front and she has a YouTube channel, is this counting as a business? Or does it need to be business expenses purchased to get the welcome offer? I’m having trouble wrapping my mind around being an Uber driver, what am I spending 6k on to get the welcome bonus. Thank you. I enjoy your content.

That sounds like a business to me! You’ll see part way down in the article, many people do put personal expenses on a business card!

How do I account for buying our Disneyland tickets on this card? Company trip? Business trip to Disney?

What if they ask for documents to prove the legal name of the business? As a sole proprietor using a social I have nothing to give them so it was denied. Any advice?

You can give you Driver’s License or SS card in that case — those are the documents you have as a sole proprietor to show your identity!

Hey Katie! I’ve been denied for my first two biz card apps this month, and I have no idea why. I called both companies and they had no answers. At 3/24, credit score 828, followed your instructions to a T, actually have legit consulting business as a side hustle…any ideas? They were Alaska Air biz card and American Air biz card.

So even calling and asking to be reconsidered, they both still said no? Alaska Air (Bank of America) can sometimes be harder for approval if you don’t have a checking account with Bank of America. At 3/24, that usually isn’t an issue but that might help for future applications with Bank of America. You can always apply again for those cards in a few months and see if anything changes. Sometimes banks will go through periods of tightening up approvals for very specific reasons. I wouldn’t worry about it too much — and just try some other business cards.

How do I determine which purchases I can put on my business card? Don’t they all need to be business related?

My understanding is that banks only include language saying it “must” be used for business expenses to follow the policy of the CARD Act. In practice, all my business cards have offers on them for many places I can use them for extra points or cash back that have nothing to do with business expenses so that leads me to believe, it isn’t firm.

On your Best Offers page, some of the business cards specify that they don’t count toward the 5/24 rule, but some don’t say anything about it (on “My take” sections). How do we know if the business card we’re applying for counts or not? Or do they all not count?

Generally business cards don’t count. I can try to go back and clarify on all the cards. The ones to look out for are Capital One cards which occasionally count. I always specify on those!

My husband and I are both registered members of our LLC, and I have an Ink card in my name. Can I refer him for an Ink with the same LLC but in his name? or will I get in trouble?

It’s a gray area, I’d personally try to refer to a different Ink than the one you have. I’m not 100% on if you’d get the referral bonus with the same EIN. But you could try and report back!

I am under 5/25 and a credit score of 800. I just applied for a Chase Ink Preferred and got the “we have to review your application” pop up, so I am assuming I am going to be denied. I do already have the Chase Business Ink Cash card. Is there any harm in applying for a card through a different lender on the same day?

you can apply same day from another lender but that review message is very common! and it’s common to get approved even after getting that, sometimes it is just a fraud check

What do you put for estimated monthly spend? I’m assuming that impacts your credit limit? I applied and put $50 (because my annual revenue for the business is only $300) and I only got approved for 5k. Which I guess is fine but will be hard to put the higher expenses to help meet the 8k welcome bonus spend (considering all of our higher expenses are happening this month)

I think it’s best to be honest! But also keep in mind that it’s pretty common for them to give you a low credit limit on business cards. You can pay for the expense, pay if off, and pay for the other expense. Don’t do that more than once as it can trigger fraud alerts. But I have had to do it before. You can also call to see if they can extend more credit.

I applied and was approved for a personal card in mid-December with Citi. I also got a Chase Preferred card in the Fall. Is it possible to be approved for a Chase Business card now or should I wait?

Yes, definitely possible!

Hi Katie! For a sole proprietor the application asks for SSN. Won’t my personal credit be pulled (not too concerned as my credit score is 820) and the 5/24 rule apply?

All applications, even for a LLC ask for your SSN. Will still see a hard pull on your credit reports but hard pulls aren’t what counts towards 5/24, it is new accounts opened. And most business cards will not show as a new account.

This was super helpful Katie! I run a small streetwear brand as a side hustle and never thought I could qualify for a business card with it. The sole proprietor tip and the screenshots of the Chase application made the whole process way less intimidating. Going to look into the Ink Business Cash card since my monthly ad spend could easily help hit that minimum spend. Thanks for breaking this down so clearly!

so glad it helped!