All content was accurate at the time of publication. Check issuer’s site for most up to date information.

Katiestraveltricks.com has partnered with CardRatings for our coverage of credit card products. Katiestraveltricks.com and CardRatings may receive a commission from our partners. American Express is a Katiestraveltricks.com advertiser. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. For Capital One products listed on this page, some of the above benefits are provided by Visa® or Mastercard® and may vary by product. See the respective Guide to Benefits for details, as terms and exclusions apply.

Spring Clean Your Credit Cards: Step by Step

Whether you’re looking to pay down debt, maximize rewards, or simplify your finances, it’s the perfect time to give your credit cards a thorough clean-up.

In this ultimate guide, we’ll take you through a step-by-step process to review, optimize, and simplify your credit card portfolio. From checking your credit report to finding cards that fit your goals, you’ll learn everything you need to make informed decisions about your credit cards.

Review your credit report

The first step in spring cleaning your credit cards is to review your credit report. This report provides valuable information about your credit history, including your payment history, credit utilization, and any outstanding debts.

Reviewing your credit report helps you identify any errors or inaccuracies that may be affecting your credit score.

Get a Free Copy of Your Reports

To get your credit report, head over to AnnualCreditReport.com. This website is the only authorized source for free credit reports from all three credit bureaus: Equifax, Experian, and TransUnion.

Tip: It’s important to use this website because it’s easy to fall for scams that offer “free” credit reports that turn out to be not free at all.

When you go to AnnualCreditReport.com, you’ll be asked to provide some personal information, including your name, address, and Social Security number. Once you’ve entered this information, you can request your credit report from one, two, or all three bureaus.

It’s best to do this on a desktop computer rather than a mobile device. This is because you’ll be able to print out your credit report more easily or save a digital copy for your records.

Check for Errors

Once you have your credit report, review it carefully for any errors or inaccuracies. If you find any errors, contact the credit bureau to dispute them. You can even file most disputes online now.

Taking the time to clean up your credit report helps ensure that your credit score accurately represents your creditworthiness and financial history.

Address any credit card debt

After reviewing your credit report, take a closer look at any outstanding credit card debt you may have. This can not only be a significant financial burden, but it also impacts your credit score negatively.

Fortunately, there are steps you can take to address this debt and improve your overall financial health.

Come up with a Plan

One option to consider is creating a debt repayment plan. This involves outlining a strategy to pay off your credit card debt over time using a consistent and manageable approach. You might prioritize paying off high-interest cards first, and then work your way through the remaining balances.

Another option is to transfer balances to cards with lower interest rates. This can help lower your monthly payments and ultimately reduce your overall debt. Keep in mind, however, that balance transfer fees may apply, and you will need to carefully consider the terms and conditions of any new cards you are considering.

Many credit card companies offer balance transfer promotions, including 0% interest for a limited time. Before jumping on a deal, however, it’s important to read the fine print and understand any fees associated with the transfer. Those fees are usually about 3%.

Make sure the promotional rate applies to the transferred balance, and not just new purchases. Additionally, make careful notes about when the promotional rate ends.

If you are struggling to make payments or need more significant assistance, consider reaching out to your credit card company to negotiate a lower interest rate or payment plan. Many companies are willing to work with customers experiencing financial difficulties.

Taking steps to reduce or eliminate credit card debt improves your overall financial health and makes it easier to manage your credit card portfolio. It also makes it easier to apply for more cards that earn more points in the future.

Protect your identity

To manage your credit cards effectively, you must also take appropriate steps to protect your identity. Credit card fraud and identity theft are rampant, and you don’t want to become a victim. Be sure to use strong, unique passwords and enable two-factor authentication wherever possible.

Set up Automatic Alerts

Another crucial step to protect your identity is to monitor your credit report by setting up automatic alerts. Here’s a video walking through how I set up alerts on my CreditKarma account.

Freeze Your Credit

All three credit bureaus offer an option to freeze your credit for free. When your credit is frozen, no one can access your credit report or open new credit in your name. Even if they have your personal information. Keeping your credit frozen is one of the best ways to protect yourself from identity theft.

When you want to apply for a new credit card or other credit (like an auto loan), simply go to the credit bureaus and remove the credit freeze. The easiest way to do this is to set up a temporary thaw or lift of the freeze.

All three bureaus offer an option to temporarily lift a credit freeze for a certain amount of time (usually a few days to a few weeks). Then your credit is automatically frozen again once the set time has passed. That gives the banks time to run your credit, and you don’t have to remember to go back and refreeze it later.

To set up a credit freeze, sign up for a free account with each bureau (Experian Equifax, and Transunion) and go to the security section in your profile.

These companies will also often try to upsell you on some sort of credit monitoring service — you don’t need that!

Inventory your current cards

Assess your current roster of cards and take a critical eye to each one, looking for both annual fees and benefits.

Make sure you know the benefits that come with each card. Some credit cards offer rental car insurance, monthly credits, extended warranty protection, or other valuable perks.

Weigh the Benefits vs the Annual Fee

Compare the benefits you’re using vs the cost of the annual fee for each card you have. If you’re getting good value from the card, it’s worth continuing to pay the annual fee.

If you’re paying annual fees but not using the benefits, it may be time to close the card or downgrade to a no annual fee option (more on this below).

Need help with a certain card? Search for a card name in our search bar (above) and for most cards with higher annual fees, we have a benefits calculator you can use!

Declutter

It’s also important to take note of which cards you’re actually using regularly. If you have a card with great rewards but find yourself never using it, it might be worth canceling to declutter your finances.

Decluttering your wallet makes room for new cards that offer better benefits.

It can hurt up your credit score to close a whole lot of cards at once, so do this carefully. We have a complete guide on closing credit cards to help you with the process.

Set up a System to Keep Track of Your Cards

If you don’t already have a system in place for keeping track of your cards, now is a great time to set one up!

Travel Freely

I think the free online app, Travel Freely (<<–that’s my affiliate code for it), is the easiest way to track your credit cards. This is essentially an interactive smart spreadsheet.

You input when you open a new card, and it will track all cards, bonus deadlines, annual fee due dates, and your 5/24 status. You can use one account to track both your personal and business cards, as well as your partner’s personal and business cards.

Travel Freely will send you automated reminders about bonus deadlines and when your annual fee is coming due. You’ll get a reminder and some suggestions for downgrading the card in case you are no longer finding value in it.

You don’t input any sensitive information into Travel Freely, just the date you signed up for a card and what the signup bonus was.

Alternative option: spreadsheet

If you want to track your cards with a spreadsheet, here is a sample credit card tracking spreadsheet you can use.

Calendar reminders

If you use a spreadsheet, you’ll want to remind yourself of deadlines. After you’ve been approved for a card, you should figure out when you have to complete your minimum spending (let’s say it’s 3 months) and then put a reminder on your calendar for 2 weeks before then to make sure you’ve completed it.

You should also set up reminders to check to make sure you’ve received bonus points and to evaluate cards after 11 months.

If you use Travel Freely, you’ll get those reminders automatically.

Check your Point Balances

Check your point balances to ensure that you’re not missing out on any rewards you’ve earned.

If you have a card that you haven’t used in a while, it’s possible that you have accrued points or rewards you don’t even know about.

The more hotel and airline points you have, the harder it is to keep track of how many points you have, where they are, and when they expire. You’ve done all this work to accumulate points, so don’t lose them because you miss an expiration date!

We recommend AwardWallet to track miles and points.

Award Wallet covers 600 loyalty programs! It can take a while to set up if you have memberships in a lot of programs, but it’s worth doing.

There is both a free and a paid option. You can track your whole family’s miles and points on Award Wallet and link your accounts. The Plus upgrade allows you to track expirations and sends alerts about points that are about to expire.

If you are concerned about security, you can choose to have the password info for all the accounts saved locally to your computer.

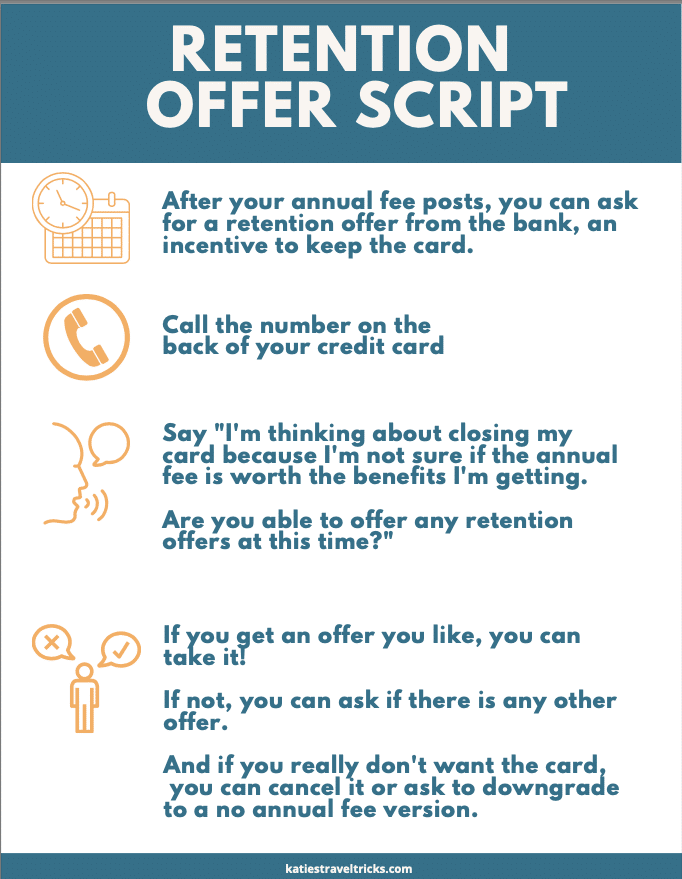

Ask for retention offers

Once you have assessed your credit cards and their applicable benefits, it’s time to take it one step further by asking for retention offers. If you have been a customer with a good payment history, it’s worth contacting your card issuer to see if they have any special offers available to keep you as a customer.

Retention offers can come in many forms, including waived annual fees, increased rewards, or even bonus points just for staying with the card. However, not all card issuers offer retention offers, and they won’t always offer them to every customer.

Not sure what to say? Follow this retention offer script below.

If you are not satisfied with the retention offer or if it’s not available, you still have another option before canceling the card.

Downgrade cards

If you aren’t offered a retention offer that suits your needs, it may be time to consider downgrading your credit card. This will allow you to keep the account open and maintain the history, without having to pay the annual fee or deal with other unwanted charges. This is sometimes referred to as a “product change” because you are changing from one credit card product to another.

Some card issuers may offer a variety of options to choose from, while others may only allow you to downgrade to a specific card–or may not give you the option at all.

Cancel cards

If you have considered all options and determined that canceling a credit card is the best course of action, keep in mind that canceling a credit card can negatively impact your credit score, especially if you have a long credit history with that card.

Your credit score takes into account the average age of your credit accounts, and closing older accounts can lower that average age and potentially damage your score.

Closing a credit card also impacts your credit utilization. If you have a lot of credit extended to you, this probably won’t make a big impact. But if you don’t have much credit or the card has a high limit, the impact could be higher.

However, if you have carefully weighed the benefits and drawbacks and determined that canceling a card is best — proceed! We regularly cancel cards and still have credit scores in the 800s.

Don’t miss the guide to closing a credit card for more information on when and how to close cards with the least impact to your credit score.

Find new cards that fit your goals

Finally, we got to the fun part, picking out cards that are better aligned with your goals.

In fact, I have a whole article all about setting travel goals and finding cards to meet them.

One of the easiest ways to put this on auto pilot is to follow my Three Year Plan.

If you already have those, look through my Best Offers page to see what hot offers match your goals!

Time to Start Cleaning Up Those Cards!

As the spring season rolls around, it’s the perfect time to give your credit cards a good old-fashioned cleaning. By reviewing your credit report, addressing any debt, and considering balance transfers, you can optimize and simplify your credit card portfolio.

Take inventory of your current cards, check their benefits, and don’t be afraid to ask for retention offers or cancel cards that no longer serve your goals.

Table of Contents

Related Posts

Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

Your pointers are really helpful. Thanks so much.

Do you want to close a card before the annual fee posts? Or after, and ask for a refund?

It doesn’t really matter either way.