All content was accurate at the time of publication. Check issuer’s site for most up to date information.

Katiestraveltricks.com has partnered with CardRatings for our coverage of credit card products. Katiestraveltricks.com and CardRatings may receive a commission from our partners. American Express is a Katiestraveltricks.com advertiser. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. For Capital One products listed on this page, some of the above benefits are provided by Visa® or Mastercard® and may vary by product. See the respective Guide to Benefits for details, as terms and exclusions apply.

What to do with Barclays American Airlines Cards

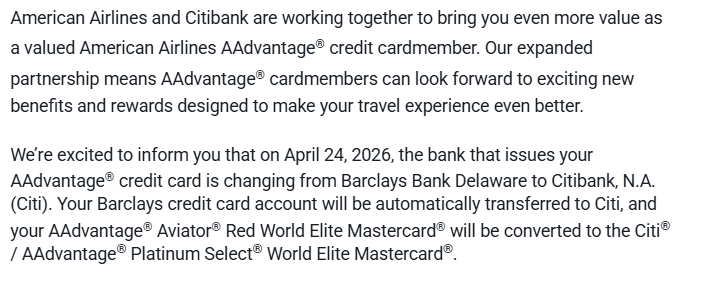

Citi is becoming the exclusive issuer for American Airlines credit cards. Barclays used to issue cards for American Airlines, but those cards are being discontinued in 2026.

On April 24, 2026, all current Barclays American Airlines cards will be converted into Citi cards. There’s still some uncertainty on how this will all play out for current customers.

If you have questions on what to do with your Barclays card before the transition to Citi, this post is for you! We’ll go over what we know and what we don’t know to help you decide on next steps. There’s no right answer for everybody, but this information can give you the tools you need to make an informed decision on what to do with your Barclays account.

Changes are Coming

Starting in late January, current Barclays customers started getting emails that looked something like this:

By now, all current Barclays customers with an American Airlines card should have gotten an email. The email will tell you what Citi card your account is converting to and some information about the transition.

What’s Happening to Current Barclays Cards?

Barclays AAdvantage cards will transition to Citi accounts on April 24, 2026. Cards won’t be mailed out until at least April 27, and could take up to eight weeks to arrive.

You’ll still be able to use your Barclays card until your new Citi card arrives.

The new Citi card you’ll get depends on which Barclays card you have. Generally, the new Citi card will be the one that most closely matches the Barclays card.

The Transition to Citi

Old and New Benefits

When you get your new card, you’ll be able to use the benefits of that card immediately.

You’ll keep some of the benefits of your current Barclays card for a limited time. These are being called “legacy benefits”. Citi has not announced when the legacy benefits will end, just that customers can still use them until they receive notice from Citi.

Annual Fee

Your annual fee will be charged on your next account anniversary. For most people, your annual fee won’t change. This is because most of the annual fees on the Barclays card and the equivalent Citi card are the same. For example, the Aviator Red and the Platinum Select both have a $99 annual fee.

For cards that are transitioning to a card with a different annual fee, it’s unclear which annual fee you’ll pay immediately after the transition. You could be charged the annual fee for the new card on your next account anniversary, or there could be a certain time period where cardmembers will pay the annual fee of their old card.

What To Do with Current Barclays Cards

For each AAdvantage card that you hold from Barclays, you have two options:

- Keep the card open and let it convert to a Citi card.

- Close the account before it converts.

Will Cards that Convert to Citi Count Towards 5/24?

It’s still unclear if a converted account will show up as a new account on your credit report and thus count towards your 5/24 count.

For those unfamiliar with the term, 5/24 is an unofficial rule but essentially means that Chase is unlikely to approve you for a new credit card if you have 5 or more new accounts showing on your credit report in the past 24 months. You can read more in our full blog post on the 5/24 rule.

Often, when a credit card account is moved over to a new bank, the account will not show up as a new account. You’ll keep your credit history and the same card number.

However, it’s possible that converted Barclays cards could get new account numbers with Citi. In that case, it will likely show up as a new credit account on your credit report. Anything that shows up as a new account on your credit report does count towards 5/24.

If You Let the Card Convert to Citi, will you Still be Eligible to Earn a Welcome Bonus on the Same Card in the Future?

This is a bit unclear as well. Some sources think that yes, you could still earn a welcome offer on the same Citi card at any time, while other sources say no, you’ll have to wait 48 months after the card converts to be eligible.

Citi has a 48-month rule for most of its credit cards. This means that you cannot earn a welcome offer on a card if you’ve earned a bonus on the same card in the last 48 months or if you’ve converted a Citi card to that card in the last 48 months. Here are the terms on the Platinum Select card directly from Citi as of February 24, 2026:

“American Airlines AAdvantage® new cardmember bonus offer not available if you received a new account bonus for or if you converted another Citi credit card account on which you earned a new account bonus into a Citi® / AAdvantage® Platinum Select® account in the last 48 months.”

As it reads currently, you would only be ineligible if you convert a Citi card into a Platinum Select card, so it should still be possible to earn a bonus if your Barclays card is converted. But it’s also possible that they could add the word Barclays to the terms at any time before or after the conversion.

What if I already have the same card from Citi?

If your Barclays card is transitioning to a card that you already have, you’ll end up with two of the same card.

You can keep both accounts open, close one, or potentially product change to a different card type.

What if It’s Been Less Than a Year Since I Opened the Barclays Card?

You still have the same options to let the card convert to Citi or close it, but having a young account does give you more to think about.

It’s never ideal to close a credit card account in less than 12 months. When a customer does this, it could give the impression that they’re only opening cards to earn rewards. Banks don’t like to see that, and it can make them hesitant to approve you for new credit cards in the future, especially if you don’t have any other accounts open with them.

Katie’s family had to make this same decision. They decided to go ahead and close their Barclays card, even though it’s only been open for 6 months. They wanted to be absolutely sure this wouldn’t add to their 5/24 count and that it wouldn’t affect future eligibility for the Citi Platinum card. It’s not ideal for the relationship with Barclays, but it’s also much easier to explain to Barclays (in a reconsideration call, for instance, for another Barclays card down the road), that the reason they closed the card was that they didn’t want to transition to Citi.

There isn’t an ideal situation here. If you’re concerned about your 5/24 status or you know you want to be eligible to earn a bonus on the Citi card in the near future, it may be worth closing your Barclays card before it converts.

Another Option: Open a Citi card before Conversion

If you’ve never had a Citi AAdvantage® Platinum Select® card before, another option is to open one before the conversion. This way, any Barclays card that converts wouldn’t really affect your eligibility. You could keep your converted Citi card open at least until you’re charged an annual fee.

This card has had a great non-affiliate offer!

non affiliate link

welcome offer:

ELEVATED OFFER!

Earn 80,000 AAdvantage® bonus miles

Earn 80,000 AAdvantage® bonus miles after $1,000 in purchases within the first 3 months of account opening. Ask a flight attendant for a code or try 539139 which we saw on a recent flight

Annual Fee:

What if My Card isn’t Converting to Citi?

A small number of people received an email stating that their Barclays American Airlines cards won’t be moving to Citi but will stay with Barclays.

If you hold an Aviator Red or Silver, those cards will be converted to a Barclays Arrival Plus Mastercard. Aviator business cards will be converted to the Barclays Juniper Business Mastercard.

The Bottom Line

Navigating bank transitions is never the most glamorous part of the points and miles hobby, but it’s exactly why staying informed pays off. There’s no universal “right” answer here. Whether you decide to close your Barclays card early to protect your 5/24 status or let it ride to see what Citi has in store, the best thing you can do is make the choice that aligns with your personal credit card strategy.

Where to go from here?

If you’re still weighing your options and want to figure out how this transition impacts your future approvals, be sure to brush up on our full guide to understanding the Chase 5/24 Rule.

Or, if you need a little motivation and a reminder of why we jump through all these hoops in the first place, head over to our Destinations page and read about Flights with Points to start dreaming up your next big trip!

Table of Contents

Related Posts

Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

I have only had my Barclays Aviator Red card open for about six months. If I close it before it converts to a Citi card, is there a chance they’ll claw back the welcome bonus?

My read on the terms is no. Here are the terms I found online which only talk about miles you’ve earned on a statement and if you close a statement in that billing cycle. My husband has already closed his, which he only had for 6 months, so I will update if anything like that happens!

“AAdvantage® Miles Forfeiture

If your Card Account is closed for any of the following

reasons, your AAdvantage® miles earned during that billing

cycle but not yet sent to American Airlines will be forfeited:

• You or any authorized user(s) on the Card Account

engages in any fraudulent or illegal activity through the use

of your Card Account.

• You, or any authorized user(s) on the Card Account engage

in any activity that is deemed to be abusive or gaming

conduct, as determined by us in our sole discretion. Abusive

or gaming activity includes, but is not limited to, obtaining

or using a card account to maximize rewards earned in a

manner that is not consistent with typical consumer activity

and/or multiple credit card account applications/openings, as

determined by us in our sole discretion.

• You or any authorized user(s) on the Card Account have

negative public record information identified.

• Your history of Card Account usage.

• You or any authorized user(s) on the Card Account violate

any of the Card Account Rewards Rules.

• Your Card Account is otherwise in default under your

Cardmember Agreement with us.

• Your AAdvantage® Account is closed.”

No they absolutely will not

Same question here, I was likely the last person in the US to be given the Aviator Red, they kept asking for more (duplicate) documents, but relented in the middle of December! Should I request the Barclays Arrival Plus World Elite Mastercard just to keep the account open a year? I already have the Citi card they’re switching us to.

Have you had the Citi card for a long time? Is this going to mess up your eligibility for that Citi card? My read on the terms is no it won’t get clawed back. Here are the terms I found online which only talk about miles you’ve earned on a statement and if you close a statement in that billing cycle.

“AAdvantage® Miles Forfeiture

If your Card Account is closed for any of the following

reasons, your AAdvantage® miles earned during that billing

cycle but not yet sent to American Airlines will be forfeited:

• You or any authorized user(s) on the Card Account

engages in any fraudulent or illegal activity through the use

of your Card Account.

• You, or any authorized user(s) on the Card Account engage

in any activity that is deemed to be abusive or gaming

conduct, as determined by us in our sole discretion. Abusive

or gaming activity includes, but is not limited to, obtaining

or using a card account to maximize rewards earned in a

manner that is not consistent with typical consumer activity

and/or multiple credit card account applications/openings, as

determined by us in our sole discretion.

• You or any authorized user(s) on the Card Account have

negative public record information identified.

• Your history of Card Account usage.

• You or any authorized user(s) on the Card Account violate

any of the Card Account Rewards Rules.

• Your Card Account is otherwise in default under your

Cardmember Agreement with us.

• Your AAdvantage® Account is closed.”